" Its not formal education but specific knowledge of something which makes you rich "

Anish Varshney, India

Anish Varshney, India

Goldman Sachs

The first major foreign brokerage to do so after the Union Budget, Goldman Sachs has upgraded the Indian equity market, citing a rebound in domestic growth in the second half of calendar year 2018 and “relatively attractive” valuations.

The Wall Street major has raised its rating on Indian shares to ‘marketweight’ in its latest Asia-Pacific quarterly outlook report. A target of 12,500 is set for the 50-stock Nifty index of the National Stock Exchange (NSE) by September 2018.

Also, analysts believe Indian corporate earnings growth may surprise modestly to the upside in 2019 and say an upward revision cycle for 2017 earnings may materialise later this year

The Wall Street major has raised its rating on Indian shares to ‘marketweight’ in its latest Asia-Pacific quarterly outlook report. A target of 12,500 is set for the 50-stock Nifty index of the National Stock Exchange (NSE) by September 2018.

Also, analysts believe Indian corporate earnings growth may surprise modestly to the upside in 2019 and say an upward revision cycle for 2017 earnings may materialise later this year

Stock Market - 5 golden Rules

When the market is upward always ' buy & sell'. when the market is in downtrend 'short & cover - that's the thumb rule

Follow ' stoploss '. never ever work without it

Make diversified investment, atleast 6 to 8 stocks. never make thematic or sectorial investment

Keep track of your investment

News and buzz in the market effects the stockmarket

Follow ' stoploss '. never ever work without it

Make diversified investment, atleast 6 to 8 stocks. never make thematic or sectorial investment

Keep track of your investment

News and buzz in the market effects the stockmarket

BROKERAGE CHARGES

Am I Rich?

· Got $2200? In this world, you’re rich. Assets (not cash) of $2200 per adult place a person in the top 50% of the world’s wealthiest.*

· If you made $1500 last year, you’re in the top 20% of the world’s income earners.**

· If you have sufficient food, decent clothes, live in a house or apartment, and have a reasonably reliable means of transportation, you are among the top 15% of the world’s wealthy. **

· Have $61,000 in assets? You’re among the richest 10% of the adults in the world.*

·If you earn $25,000 or more annually, you are in the top 10% of the world’s income-earners.***

· If you have any money saved, a hobby that requires some equipment or supplies, a variety of clothes in your closet, two cars (in any condition), and live in your own home, you are in the top 5% of the world’s wealthy. **

·If you earn more than $50,000 annually, you are in the top 1% of the world’s income earners.***

· If you have more than $500,000 in assets, you’re part of the richest 1% of the world.*

· Got $2200? In this world, you’re rich. Assets (not cash) of $2200 per adult place a person in the top 50% of the world’s wealthiest.*

· If you made $1500 last year, you’re in the top 20% of the world’s income earners.**

· If you have sufficient food, decent clothes, live in a house or apartment, and have a reasonably reliable means of transportation, you are among the top 15% of the world’s wealthy. **

· Have $61,000 in assets? You’re among the richest 10% of the adults in the world.*

·If you earn $25,000 or more annually, you are in the top 10% of the world’s income-earners.***

· If you have any money saved, a hobby that requires some equipment or supplies, a variety of clothes in your closet, two cars (in any condition), and live in your own home, you are in the top 5% of the world’s wealthy. **

·If you earn more than $50,000 annually, you are in the top 1% of the world’s income earners.***

· If you have more than $500,000 in assets, you’re part of the richest 1% of the world.*

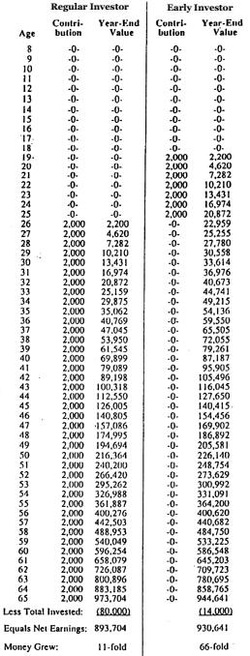

Compounding only works through time

Pan Card

PAN is a 10 digit alpha numeric number, where the first 5 characters are letters, the next 4 numbers and the last one a letter again. These 10 characters can bedivided in five parts as can be seen below.

1. First three characters are alphabetic series running from AAA to ZZZ

2. Fourth character of PAN represents the status of the PAN holder.

• C — Company

• P — Person

• H — HUF(Hindu Undivided Family)

• F — Firm

• A — Association of Persons (AOP)

• T — AOP (Trust)

• B — Body of Individuals (BOI)

• L — Local Authority

• J — Artificial Juridical Person

• G — Government

3. Fifth character represents first character of the PAN holder’s last name/surname.

4. Next four characters are sequential number running from 0001 to 9999.

5. Last character in the PAN is an alphabetic check digit.